Roth IRA Calculator: Understanding your retirement savings potential is crucial, and a Roth IRA calculator can be an invaluable tool. These online resources simplify complex calculations, allowing individuals to project their future retirement nest egg based on various factors such as contribution amounts, investment growth rates, and withdrawal timelines. Different calculators offer varying features, making it important to understand their capabilities before making financial decisions.

This analysis explores the functionality of Roth IRA calculators, highlighting key input variables and the interpretation of results. We’ll examine the strengths and limitations of these tools, comparing different calculators and offering insights into how to use them effectively for informed retirement planning. The goal is to empower readers to make sound financial choices based on accurate projections and a clear understanding of the potential impacts of their savings strategies.

Understanding Roth IRA Calculators

Roth IRA calculators are valuable tools for individuals planning for retirement. They provide estimates of future Roth IRA balances, considering factors like contributions, investment growth, and tax implications. Understanding how these calculators work and interpreting their results is crucial for effective retirement planning.

Roth IRA Calculator Functionality and Types

Source: theskilledinvestor.com

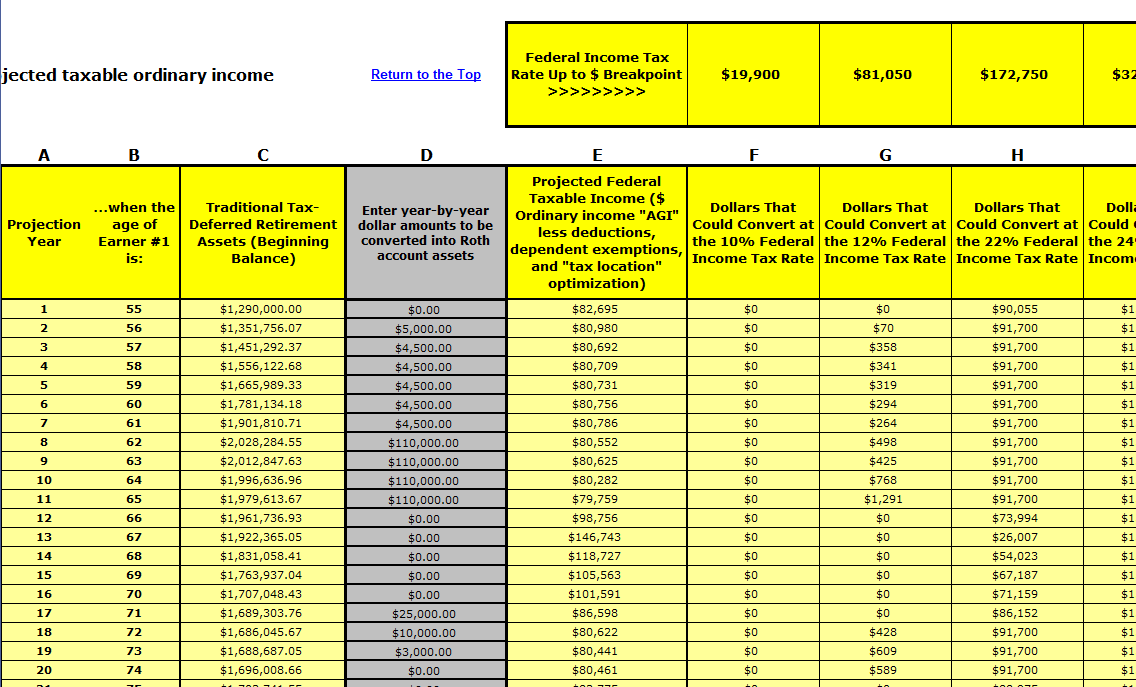

A Roth IRA calculator estimates the potential growth of your Roth IRA account over time. It takes various inputs, such as annual contributions, expected investment returns, and your age, to project your account balance at retirement. Online, you’ll find various types, ranging from simple calculators offering basic projections to more sophisticated ones incorporating advanced features like tax adjustments and variable contribution amounts.

Some calculators focus solely on Roth IRAs, while others may offer comparisons with Traditional IRAs.

Comparison of Roth IRA Calculators

Several popular online Roth IRA calculators offer varying levels of detail and functionality. Let’s compare three hypothetical examples:

| Feature | Calculator A | Calculator B | Calculator C |

|---|---|---|---|

| Contribution Limits | Yes, with annual updates | Yes, user-defined | Yes, with historical data |

| Tax Implications | Simplified estimates | Detailed breakdown | Detailed breakdown, including potential tax bracket changes |

| Withdrawal Rules | Basic summary | Detailed explanation | Interactive guide with scenarios |

| Investment Growth Rate Options | Fixed rate | Variable rate, with multiple scenarios | Variable rate, with custom scenarios and market index tracking |

Key Input Variables for Roth IRA Calculations: Roth Ira Calculator

Accurate Roth IRA projections depend on several key input variables. Understanding the impact of each variable is essential for making informed decisions.

Impact of Input Variables

The accuracy of a Roth IRA projection heavily relies on the accuracy of the input variables. These variables significantly impact the final calculation. Inaccurate inputs can lead to misleading projections. Let’s explore the most important variables.

- Age: Determines the investment timeframe and the number of years for compounding growth.

- Income: Influences the contribution limits and potential tax benefits.

- Contribution Amount: Directly impacts the initial investment and subsequent growth.

- Investment Growth Rate: A crucial factor determining the overall return on investment. Historical market data can provide guidance, but future returns are uncertain.

Data Sources for Input Variables

Reliable data sources are crucial for accurate projections. Information on contribution limits can be found on the IRS website. Investment growth rates can be estimated using historical market data from reputable sources like financial news websites or investment firms. Personal income information is readily available from tax returns or pay stubs.

Examples of Input Value Impact

- Scenario 1: A 30-year-old contributing $6,000 annually with a 7% growth rate will have a significantly larger balance at retirement than a 50-year-old contributing the same amount.

- Scenario 2: Increasing the annual contribution by even $1,000 can substantially increase the final balance due to the power of compounding.

- Scenario 3: A higher assumed growth rate (e.g., 9% vs. 7%) will result in a much larger projected balance, although higher growth rates are associated with higher risk.

Interpreting Roth IRA Calculator Results

Understanding the output of a Roth IRA calculator is crucial for making informed decisions. Key metrics to focus on include the projected future value of your Roth IRA at retirement and the potential for tax-free withdrawals.

Step-by-Step Guide to Using a Roth IRA Calculator

- Gather necessary information: Determine your age, annual contribution amount, expected investment return rate, and contribution timeframe.

- Input the data: Enter the gathered information into the chosen Roth IRA calculator.

- Review the results: Carefully examine the projected future value of your Roth IRA at retirement.

- Analyze the tax implications: Understand how the Roth IRA structure affects your taxes in both the contribution and withdrawal phases.

- Adjust variables: Experiment with different input values to assess their impact on the final balance. This helps you understand the sensitivity of the projections to changes in your assumptions.

Applying Calculator Projections to Financial Planning, Roth Ira Calculator

Use the calculator’s projections to assess if your current savings plan is sufficient to meet your retirement goals. If the projected balance falls short, you may need to increase your contributions, adjust your investment strategy, or reassess your retirement goals.

Limitations and Considerations of Roth IRA Calculators

Roth IRA calculators provide valuable estimates, but it’s essential to acknowledge their limitations. The projections are based on assumptions that may not perfectly reflect reality.

Potential Inaccuracies and Biases

- Market Volatility: Calculators typically assume a consistent rate of return, which may not accurately reflect the fluctuating nature of the stock market.

- Inflation: The projections may not adequately account for the erosion of purchasing power due to inflation.

- Tax Law Changes: Future changes in tax laws could significantly impact the tax benefits of a Roth IRA.

- Unforeseen Expenses: The calculator does not account for unexpected life events that might require withdrawals from the IRA.

- Simplified Investment Models: Most calculators use simplified models of investment growth, ignoring factors like transaction costs and fees.

Visualizing Roth IRA Growth

Imagine a line graph charting the growth of a Roth IRA over time. The x-axis represents the years, from the initial investment to retirement (e.g., 30 years). The y-axis represents the account balance, starting at the initial investment and increasing over time. Multiple lines could represent different scenarios: a conservative investment strategy (e.g., 5% annual growth), a moderate strategy (e.g., 7%), and an aggressive strategy (e.g., 9%).

The graph clearly shows how the final balance increases dramatically with higher growth rates and longer time horizons. Key data points would include the balance at 5-year intervals and the final balance at retirement for each scenario. The graph would visually demonstrate the power of compounding and the impact of different investment approaches on long-term growth.

Planning your retirement with a Roth IRA Calculator can be surprisingly complex, requiring careful consideration of various factors. However, some life choices are far more unpredictable, like the behind-the-scenes drama revealed in shocking secrets of the anchorman 2 cast you haven’t heard exposed the secrets you cant miss. Ultimately, securing your financial future through wise Roth IRA planning remains a crucial step, regardless of Hollywood headlines.

Roth IRA vs. Traditional IRA: Calculator Comparison

Comparing Roth and Traditional IRA calculators highlights the key differences in tax implications and projected balances. For the same individual and contribution amounts, a Roth IRA calculator will show a lower balance initially (due to taxes paid upfront) but potentially a higher after-tax balance at retirement, while a Traditional IRA calculator will show a higher initial balance but potentially a lower after-tax balance at retirement due to taxes owed upon withdrawal.

Comparison Table

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax Treatment of Contributions | Taxed now | Tax-deductible now |

| Tax Treatment of Withdrawals | Tax-free in retirement | Taxed in retirement |

| Projected Balance at Retirement (Example) | $500,000 (after-tax) | $450,000 (before-tax, potentially lower after-tax) |

| Factors Influencing Choice | Current tax bracket, expected future tax bracket, risk tolerance | Current tax bracket, expected future tax bracket, risk tolerance |

Final Review

Ultimately, a Roth IRA calculator serves as a powerful planning tool, but it’s essential to remember that projections are just estimates. Market volatility, changes in tax laws, and individual circumstances can all influence actual retirement outcomes. While these calculators offer valuable insights, they should be used in conjunction with professional financial advice to create a comprehensive and personalized retirement strategy that aligns with individual risk tolerance and long-term goals.

Careful planning and informed decision-making are key to securing a comfortable financial future.